Rising interest rates act as a reality check

VC-backed spoiled kids are crying

Hey, there’s a bubble

Interest rates act on financial valuations the way gravity acts on matter." This isn't my quote; it's Warren Buffett's. If you're unfamiliar with him, I encourage you to check out his Wikipedia page.

For small business owners, the gravitational pull of interest rates might exert an even stronger force on your operations. Can you operate without borrowing money? Have you relied heavily on leverage? Do your clients depend on leverage? Let's dig into these questions and explore how you can navigate the current economic context – and, hopefully, adapt to it.

Let's rent on Airbnb, buddy

Before digging deeper, let's consider the broader financial backdrop. Interest rates have remained historically low for decades, and this trend crazingly intensified post-COVID. The US Federal Reserve, along with central banks worldwide, further reduced rates and implemented quantitative easing measures to stimulate demand.

You don’t need a rocket science degree to understand that if borrowing money is cheap and easily accessible, many people will try to do it, and yet a significant part of them will still be unable to generate profits: it’s the law of business1. If it were easy to make money, everyone would do it. This doesn't really matter as long as refinancing is possible and cheap: this led to a false growth fueled by free money, and to leveraged financial structures dependent on once-in-a-lifetime economic parameters:

Low interest rates on both the supplier and consumer side, leading to an explosive offer-demand effect and eventually leading to greed on the supplier side, with more supply than demand.

Exceptionally strong incentive to invest in non-profitable companies because savings don't yield any return. The VC market has become a giant joke filled with idiotic deals.

Explosive growth of real estate in some emerging markets, with unique currency exchange rates leading to new potential buyers with unprecedented purchasing power.

The world's age-old fallacy of thinking that what is true now will be true forever, leading to the development of non-sustainable business models.

While quantitative easing policies aimed to stabilize economies, they inadvertently gave rise to localized—and potentially globalized—financial bubbles. More interestingly, a new generation of entrepreneurs has emerged. Fueled by easily accessible capital, many have lost sight of the age-old business tenet: the pursuit of profits and net incomes.

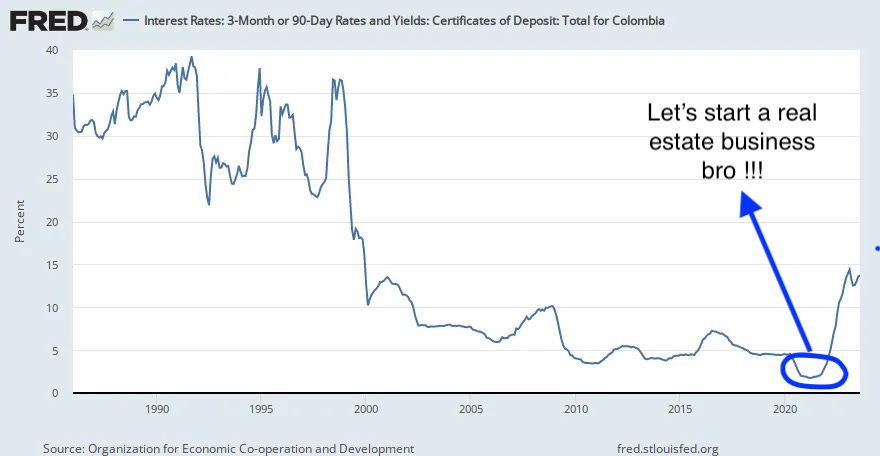

Below is a graph of historical interest rates in Colombia. You can observe a significant easing post-COVID, representing a highly unusual situation from a historical perspective. I've added a slightly ironic comment regarding the new breed that has inundated the real estate market in recent years. Any random idiot would buy and profit effortlessly from a "rent-on-Airbnb" scheme. Many of them are quickly going broke, with no savings since they spent it all on frivolous clothes and additional apartments: greed always leads you to the grave.

You got the idea, and you understood my point. Now, what does that mean for your small business? Let's ask the relevant questions so you can see if you are exposed.

Liquor, ladies, leverage

Charlie Munger's "Three L's" metaphor — Liquor, Ladies, and Leverage — is a cautionary tale. While the dangers of "Liquor" and "Ladies" are well-known, "Leverage" is the more complex trap. It's not just about borrowing too much; it's also the temptation of low interest rates and the self-fulfilling belief that refinancing will always be possible at no cost. When those rates rise for a prolonged period, the costs compound quickly. Sure, the "Three L's" might sound old-fashioned and a bit sexist, but they're catchy enough to mention and applicable to anyone. Also, if you don’t know Charlie Munger, check his book and his philosophy.

Let’s come back to your small venture : the first question to ask is: Are you leveraged, and does the industry you operate in rely on low interest rates and easy money to thrive? If the answers to both these questions are "yes," then you should take a moment to sit down, breathe, and consider whether it might be time to face reality restructure, or just leave with dignity2. Here are two cases:

Airbnb rental speculation: John, with no prior investment experience and not being particularly literate, loves exploring new ways to make money on Instagram and TikTok. John had purchased three properties3 in a popular tourist destination to list them on Airbnb. During the times of low interest rates, he could to secure mortgages with minimal monthly payments. The properties were often booked, providing John with a substantial income over his expenses and generating appealing profits. However, when interest rates began to rise, the number of tourists seeking Airbnb accommodations decreased as travel became more expensive4, and refinancing became impossible or too costly. With decreased revenue and potentially increase expenses, John finds himself struggling to cover his mortgages and facing a tragic(omic) blow-up. The once-lucrative Airbnb strategy quickly turned into a financial nightmare, sending John back to where he belongs in the business food chain: among short-term suckers soon-to-be-broke.

Cash-burning Tech startups: Bob founded a tech startup, developing a cutting-edge SaaS tool. In the early days of his company, venture capitalists were eager to blindly invest the abundance of free money available from pension funds. The ambitious venture didn't turn a profit in the first few years, which was expected. As interest rates climbed, VCs learned tough lessons and lacked funds to invest as their partners preferred good old savings. With Bob's startup having no path to profitability and burdened with fat operating expenses, he had no other options than to restructure harshly or close down. The tech world's "grow fast, profit later" model was suddenly under immense pressure.

Now, let’s say you don't fit into any of those fairly dystopic examples and actually run a potentially sustainable business, or you are already profitable. Then, your best days may be just around the corner. Low interest rates create competitors that can distort market incentives; these competitors won't be able to sustain themselves, and your traditional company has brighter days ahead.

Another consequence of rising interest rates is a potential shift in client behavior, which can favor more established, less trendy businesses. As both money and time become more valuable, clients, be they businesses or consumers, often become more selective and cautious, focusing on essential needs.

In a low-interest-rate environment, people are easily drawn to the latest trends, driven by a fear of missing out, and are prone to silly financial behaviors fueled by easy leverage. When these conditions are no longer in place, your cautious business approach suddenly stands out as a safe haven.

Save your cash,

Watch your costs,

Keep the faith.

97% of businesses never make it, they just die quicker when interest rates are high.

Everyone fails, that’s no big deal.

My good French buddy Jeremy told me he met a gringo with 16 properties … there’s a bubble.

Needless to say, a significant portion of travelers used leverage to buy tickets and seek properties they then bought with more leverage. Leverage, leverage everywhere.